A red herring in a business prospectus typically refers to preliminary financial statements or forward-looking statements that may be misleading or divert investor attention from potential risks. For instance, a company might highlight optimistic revenue growth projections without adequately disclosing underlying liabilities or market challenges. This tactic can create an inflated perception of the company's financial health, which influences investor decisions based on incomplete or skewed information. In prospectuses, red herrings often manifest as vague descriptions of competitive advantages or future product pipelines that lack detailed data or credible backing. Entities may emphasize recent successes or high-profile partnerships while minimizing discussion of financial losses or regulatory issues. Such practices can impact due diligence by obscuring critical data points necessary for accurate risk assessment.

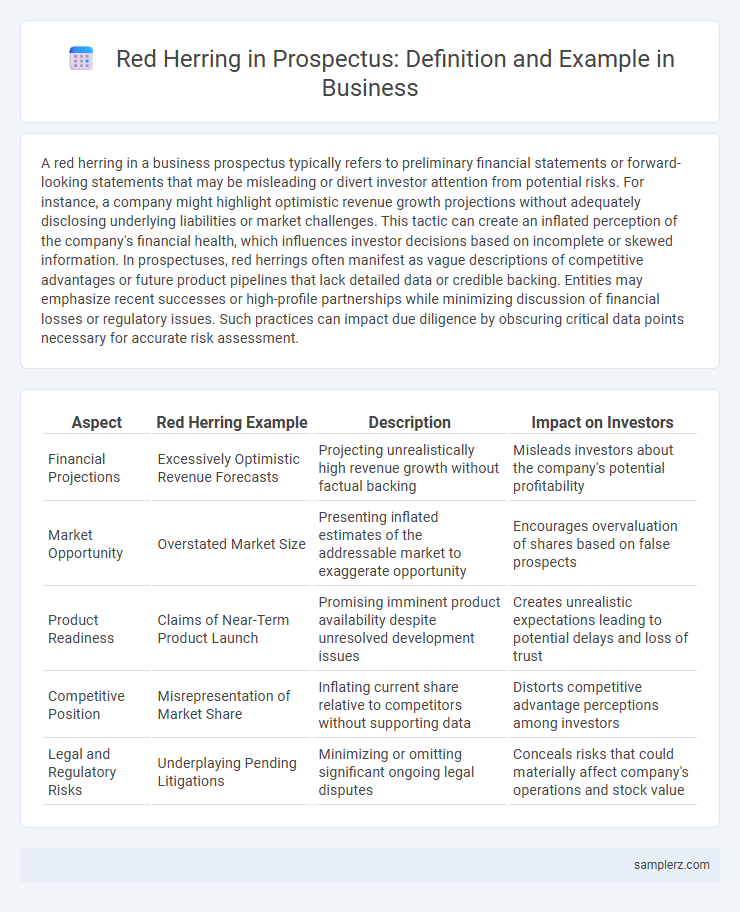

Table of Comparison

| Aspect | Red Herring Example | Description | Impact on Investors |

|---|---|---|---|

| Financial Projections | Excessively Optimistic Revenue Forecasts | Projecting unrealistically high revenue growth without factual backing | Misleads investors about the company's potential profitability |

| Market Opportunity | Overstated Market Size | Presenting inflated estimates of the addressable market to exaggerate opportunity | Encourages overvaluation of shares based on false prospects |

| Product Readiness | Claims of Near-Term Product Launch | Promising imminent product availability despite unresolved development issues | Creates unrealistic expectations leading to potential delays and loss of trust |

| Competitive Position | Misrepresentation of Market Share | Inflating current share relative to competitors without supporting data | Distorts competitive advantage perceptions among investors |

| Legal and Regulatory Risks | Underplaying Pending Litigations | Minimizing or omitting significant ongoing legal disputes | Conceals risks that could materially affect company's operations and stock value |

Understanding the Red Herring in a Business Prospectus

A red herring in a business prospectus refers to the preliminary version of the document that includes essential information about an upcoming securities offering but omits key details like the price and volume of shares, highlighting regulatory compliance during the SEC review process. This initial prospectus acts as a legal placeholder, allowing companies to generate investor interest while ensuring transparency about business risks, financial status, and operational details. Understanding the red herring is crucial for investors to evaluate the fundamentals before final offering terms, enhancing informed decision-making in capital markets.

Key Elements of a Red Herring Document

A red herring prospectus prominently features a preliminary offering price range, detailed risk factors, and company financial statements to inform potential investors before the final pricing is set. It excludes the exact number of shares to be issued and the final offer price, which are disclosed only in the final prospectus. This document is essential in complying with regulatory requirements while providing a comprehensive overview of the business's potential and risks.

Real-World Red Herring Prospectus Examples

A red herring prospectus, often seen in IPO filings, includes incomplete or preliminary financial data without final pricing details, as exemplified by companies like Uber during its 2019 public offering. This document highlights growth metrics and market potential while withholding specific share price and underwriting information to comply with regulatory review processes. Real-world examples illustrate how red herrings manage investor expectations by providing essential business insights without full disclosure until SEC approval is attained.

How Companies Use Red Herrings in IPOs

Companies use red herrings in IPO prospectuses to provide preliminary financial data and business strategies without finalizing critical details such as share price or number of shares. This draft document allows firms to gauge investor interest and comply with SEC regulations while retaining flexibility to adjust terms before the official registration statement. The red herring includes risk factors and company disclaimers, signaling potential uncertainties to investors during the early stage of the public offering process.

Regulatory Requirements for Red Herring Prospectuses

A red herring prospectus is a preliminary registration document for an initial public offering (IPO) that contains essential information about the company's business and financial status but excludes key details like the offer price and number of shares. Regulatory requirements mandate that red herring prospectuses include risk factors, use of proceeds, and detailed business descriptions, ensuring transparency and investor protection before the final prospectus is issued. Compliance with securities laws, such as those enforced by the SEC in the United States, requires that these documents avoid misleading statements and provide accurate disclosures to facilitate informed investment decisions.

Common Misconceptions about Red Herring Documents

Red Herring prospectuses often cause confusion by being mistaken for final offering documents when they are actually preliminary and lack complete details like the exact number of shares or price. Common misconceptions include assuming that the information is definitive or that investment decisions should be based on it, although it primarily serves to inform potential investors of the offering's general terms pending regulatory approval. Understanding that the Red Herring does not guarantee the final terms prevents misinterpretation and helps maintain compliance with securities regulations.

Risks Highlighted in Red Herring Examples

A red herring prospectus typically emphasizes risks such as market volatility, regulatory changes, and financial uncertainties that could impact the company's performance. Common risks highlighted include potential fluctuations in revenue streams, dependency on key management personnel, and possible delays in project execution. Investors are advised to carefully evaluate these risk factors before making investment decisions.

Differences Between Red Herring and Final Prospectus

A red herring prospectus is an initial document filed with the SEC during an IPO, containing preliminary financial details without the final price or share quantity. In contrast, the final prospectus includes definitive information such as the offering price, exact number of shares, and the effective registration date, making it legally binding for investors. The red herring serves to generate interest while the final prospectus is used for actual investment decisions.

Analyzing Disclosures in Red Herring Prospectuses

Analyzing disclosures in red herring prospectuses reveals preliminary financial data and risk factors that highlight the issuer's potential market challenges without finalizing the offering details. These documents typically omit the exact price and number of shares, emphasizing material business risks such as operational uncertainties, legal proceedings, or market volatility to inform investors during the registration process. Careful scrutiny of these disclosures aids investors in assessing the speculative nature and underlying risks before the prospectus becomes effective.

Best Practices for Reviewing a Red Herring Prospectus

A red herring prospectus often includes preliminary financial data and risk factors designed to attract investor interest while disclaiming full accuracy until finalized. Best practices for reviewing such a document involve meticulously verifying disclosed liabilities, evaluating the clarity of risk disclosures, and cross-checking the offering details with regulatory filings. Ensuring the absence of misleading statements and assessing the completeness of financial statements are critical to making informed investment decisions.

example of red herring in prospectus Infographic